On paper, African currency volatility looks like a technical problem: you model it in your entry assumptions, maybe budget for a haircut on exit, and move on. But in practice, it shapes the investment thesis from day one.

Take entry valuations. A company priced at 10x EBITDA in local currency may suddenly look like 12x overnight if the shilling weakens before close. That shift alone can destroy a carefully constructed investment case. During ownership, earnings can grow double digits in local terms but still shrink in dollars. And at exit, LPs may find that strong operating performance is masked by translation losses when converting to USD or EUR.

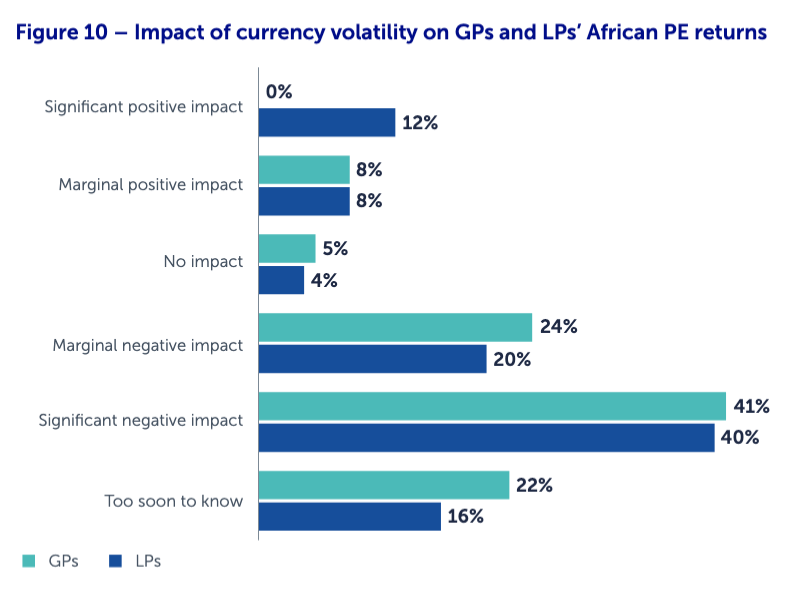

Here’s an interesting reality check: according to AVCA’s Currency Risk in Africa Report (2023), 90% of GPs and 71% of LPs said that the economic performance of African countries was the main factor behind rising currency risk. That ranked higher than COVID-driven macroeconomic shocks (72% of GPs, 50% of LPs) or even political stability concerns (52% of GPs, 57% of LPs).

In other words, the very foundation of FX volatility isn’t just politics or global downturns, it’s the day-to-day economic engines of African markets themselves. And yet, many funds still treat currency exposure within private equity risk management like an afterthought, something to patch over in the financial model rather than designing resilience into their investment approach from the ground up.

My take? FX risk isn’t just an afterthought, it’s a filter. The best managers don’t see volatility as random punishment, they treat it as an X-ray. It reveals which businesses are overexposed and which have the DNA to thrive under pressure.

That’s why at Lighthouse we believe the question isn’t, “How do we avoid FX volatility?” (you can’t). The smarter question is, “How do we build portfolio companies that still create dollar returns despite it?” In other words, we use FX stress tests not just for financial models, but for operating models. If a company’s leadership, pricing, and systems can’t handle a 20% devaluation in year one, it probably won’t make it through the decade.

Currency swings are not just math they’re management. And for LPs, backing GPs who understand that difference is the real hedge

Education

-MBA in Finance and Entrepreneurship, Bond University, Australia

-BCom in Finance & Economics, University of the Witwatersrand, South Africa

-Advanced Diploma in Bank Credit & Risk Management, Damelin School of Banking

- Managing Currency Risk in African Private Equity - August 20, 2025

- African Private Equity: Strategy, Investment Thesis & Operational Edge - August 13, 2025